You are receiving this communication because you are a client of or have expressed interest in NorthCoast Asset Management

May 2023

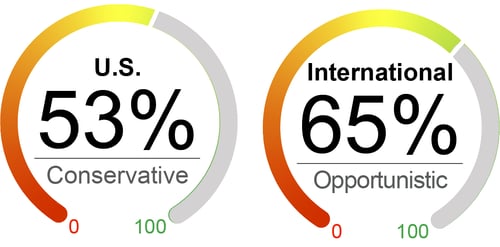

Current Equity Exposure

Major equity indexes ended the month of April higher: the Dow and the S&P 500 gained 2.6% and 1.6%, respectively, while the technology-heavy Nasdaq was flat (up 0.07%) for the month. We stayed underweight U.S. equities as we believe the risks remain skewed toward the downside with tightening financial conditions, macro risks, deteriorating economic leading indicators, and corporate earnings pressure. Notably, we increased our international equity exposure from 53% to 65% as we see recent activity data pointing to the upside for Europe and China. April PMI data in Europe and the U.K. painted an optimistic picture of business activity driven by the robust service sector. China’s recovery remains on track, with Q1 GDP surprising to the upside and leading indicators suggesting upside dynamics.

The Factors

Valuation

Valuation metrics for equity remained negative. P/E increased slightly from 19.7 at the end of March to 19.9 at the end of April.

Forward P/E increased to 19.0 at the end of April from 18.8 at the end of March.

Inflation-adjusted valuation metrics continued to be negative.

Equity valuation metrics relative to bonds remain negative with high bond yields .

Sentiment

U.S. manufacturing activity contracted for the fifth month, with the ISM manufacturing index falling to 46.3 in March from 47.7 in February.

University of Michigan Consumer Confidence Index remained weak at 63.5, battered by continuing high inflation, recession fears, and financial market stress.

The NAHB index inched up 1 point in April but remained below neutral level at 45 .

Technical

Technical indicators were positive, with increasing momentum signals outweighing neutral reversal signals.

The S&P 500 was 5% above its 200-day moving average, 4% above the 100-day average, and 3% above the 50-day average.

The VIX index decreased and settled at 15.8. The low volatility is largely driven by technical factors.

Macroeconomic

Nonfarm payrolls rose by 236,000 in March, in line with expectations. The four-week moving average of initial jobless claims increased to 236,000 as of April 22.

Retail sales fell 1% after dropping 0.2% in February, with slow growth of real income and spending shifting from goods to services.

U.S. industrial production expanded 0.4% in March.

What's Driving the Markets?

Slower economy and signs of softness in the labor market: U.S. GDP grew by a disappointing 1.1% over the first quarter. Leading indicators such as the deep inversion of the yield curve and Conference Board Leading Economic Index also indicate a looming downturn in the economy. While the robustness of the labor market has supported the U.S. economy so far, recent data suggested some emerging signs of weakness. The initial jobless claims showed an upward trend since the beginning of February, and the continuing claims jumped to their highest level since November 2021. The new signs of labor market softness were taken by some investors as welcome news as it could lead to slowing wage growth and ultimately less restrictive Fed policy. However, we still expect another 25-basis point hike from the Fed in their May meeting as core inflation remained elevated, and March’s FOMC minutes demonstrated the Fed’s confidence in the soundness of the banking system.

Debt ceiling in focus again: In the wake of weaker-than-anticipated tax receipts so far, fears intensified that the U.S. Treasury will reach the “x-date” (the date it runs out of cash to pay the government’s bills on time) as soon as early June. We anticipate the “x-date” to be in late July as non-withheld tax payments are due around June 15 and another tranche of extraordinary measures will provide Treasury with a few more weeks of cash. We believe that it is likely that the impasse will eventually be resolved. Even if the debt ceiling is breached, the outcome will be disruptive but not disastrous, as the situation usually does not last more than a few weeks. However, we anticipate this recurring issue will begin making headlines in the next few months and could potentially generate market volatility including a stock market selloff, a wider credit spread, and a falling U.S. dollar.

Quarterly earnings: Earnings reports have surprised to the upside so far: among 53% of S&P 500 companies reporting actual results, 79% of them have reported a positive EPS surprise, and 74% have reported a positive revenue surprise. The equity market was encouraged by better-than-expected Q1 earnings results from tech companies including Microsoft, Alphabet, and Meta. However, the blended earnings decline for the S&P 500 was -3.7%, and the S&P MidCap 400 Index suffered a more significant year-over-year aggregate decrease in earnings. Companies continued to struggle as margin pressures were high, with slowing sales, elevated input costs, and high wages.

.

As of 4/30/23. Data provided by Bloomberg, NorthCoast Asset Management, Federal Reserve History.

1 The NorthCoast Navigator is a market barometer displaying NorthCoast's current U.S. and international equity exposure and outlook. This aggregate metric is determined by multiple data points across four broad market-moving dimensions: Technical, Sentiment, Macroeconomic, and Valuation. The daily result determines equity exposure in our tactical strategies.

NorthCoast Asset Management is a d/b/a of, and investment advisory services are offered through, Connectus Wealth, LLC, an investment adviser registered with the United States Securities and Exchange Commission (SEC). Registration with the SEC or any state securities authority does not imply a certain level of skill or training. More information about Connectus can be found at www.connectuswealth.com.

NorthCoast and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

PAST PERFORMANCE DOES NOT GUARANTEE OR INDICATE FUTURE RESULTS.

This material should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or investment products or to adopt any investment strategy. The reader should not assume that any investments in companies, securities, sectors, strategies and/or markets identified or described herein were or will be profitable and no representation is made that any investor will or is likely to achieve results comparable to those shown or will make any profit or will be able to avoid incurring substantial losses. Performance differences for certain investors may occur due to various factors, including timing of investment. Investment return will fluctuate and may be volatile, especially over short time horizons.

INVESTING ENTAILS RISKS, INCLUDING POSSIBLE LOSS OF SOME OR ALL OF THE INVESTOR'S PRINCIPAL.

The investment views and market opinions/analyses expressed herein may not reflect those of NorthCoast as a whole and different views may be expressed based on different investment styles, objectives, views or philosophies. To the extent that these materials contain statements about the future, such statements are forward looking and subject to a number of risks and uncertainties.

NorthCoast Asset Management

One Greenwich Office Park, Greenwich, CT 06831, United States