You are receiving this communication because you have expressed interest in NorthCoast Asset Management

June 2023

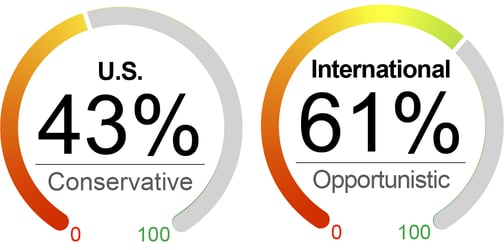

Current Equity Exposure

Major U.S. equity indexes ended mixed for May: the Dow lost 3.2%, the S&P 500 was flat (+0.4%), and the technology-heavy Nasdaq gained 5.9% for the month. The ongoing negotiations to lift the U.S. debt ceiling reignited market volatility toward the end of the month. Given the tightening of financial conditions, a heightened risk of recession, corporate margins pressure and the stretched valuations, we find the risk-reward prospect for equity still unattractive. Moreover, we believe the equity market's expectations of a substantial Fed pivot during the latter half of the year, including a rate cut of nearly 60pbs, are overly optimistic. Given this backdrop, we maintained a conservative stance in equities, trimming our U.S. equity exposure from 53% to 43%, and our international exposure from 65% to 61% during the month.

The Factors

Valuation

Valuation metrics for equity remained negative. P/E increased slightly from 19.9 at the end of April to 20.0 at the end of May.

Forward P/E remained flat at 19.1 at the end of May.

Inflation-adjusted valuation metrics continued to be negative.

Equity valuation metrics relative to bonds remained negative with high bond yields.

Sentiment

U.S. manufacturing activity contracted for the sixth month, with the ISM manufacturing index remaining below the neutral threshold at 47.7 in April.

The University of Michigan Consumer Confidence Index remained weak at 59.2, with persistently high inflation, high interest rates, recession fears, and higher layoffs.

The NAHB index climbed 5 points in May to reach the neutral level of 50.

Technical

Technical indicators were positive, with increasing momentum and fear signals outweighing negative reversal signals.

The S&P 500 was 5% above its 200-day moving average, 3% above the 100-day average, and 2% above the 50-day average.

The VIX index increased and settled at 17.9. The ongoing U.S. debt ceiling negotiation reignited market volatility toward the end of the month.

Macroeconomic

Nonfarm payrolls rose by 253,000 in March, higher than expectations. The four-week moving average of initial jobless claims decreased to 231,750 as of May 20.

Retail sales grew 0.4% after dropping 0.7% in March, with part of the growth due to price increases.

U.S. industrial production expanded by 0.5% in April.

What's Driving the Markets?

The Debt Ceiling deal has modest growth impact: The debt ceiling agreement outlined in the “Fiscal Responsibility Act” negotiated by President Biden and House Speaker McCarthy gained approval from the House on 5/31. This agreement will eliminate much uncertainty surrounding the approaching debt limit deadline, though it still needs to be passed by the Senate on June 2. The bill, if passed, will suspend the debt limit until 2025, mainly by imposing restrictions on discretionary spending for the next two years. It also introduces various policy changes that will impact areas such as student loans, work requirements for certain government benefit recipients, and the National Environment Policy Act. We believe that the spending deal would create very modest headwinds to U.S. growth. It is anticipated that it could lead to a reduction in real GDP by approximately 0.1-0.2%, a decrease of about 120,000 jobs in nonfarm employment, and an uptick of 0.1% in the unemployment rate in 2024.

Fed nearing pause but keeps rates high: As widely anticipated, the Federal Open Market Committee has raised the federal funds rate for the 10th consecutive meeting in May, bringing the target range of the Fed funds rate to 5% to 5.25%. We see the Fed nearing a pause in rate hikes based on several factors: 1) The notable exclusion of the committee's statement that "additional policy firming may be appropriate" suggests that the FOMC views the May rate increase as potentially the last one of this tightening cycle, 2) Monetary policies usually work with time lags, indicating a continuing drag on the economy from previous rate hikes, and 3) Recent developments in the banking sector are expected to result in tighter credit conditions, which means that the Fed might need to do less tightening for its monetary policy. However, we do not anticipate a rate cut to occur until early 2024. This cautious stance is justified by continuing elevated core inflation as well as recent overall economic data, especially the labor market and consumer spending, which continue to hold up better than consensus forecasts.

Inflation is on a downward path but expectations high: Both the headline and core CPI rose by 0.4% in April. On a year-over-year basis, the headline and core CPIs rose 4.9% and 5.5%, respectively. This latest data indicates significant progress in tackling inflation in the U.S., with key pockets of disinflation within core services excluding rent of shelter. Inflation is on a downward trajectory, yet the uptick in consumer inflation expectations and wage growth raises could be concerning for the Federal Reserve. One-year inflation expectations have risen to 4.2% from the recent low of 3.6% in March, while the 5-year ahead expectations have reached 3.1%, compared with four straight months at 2.9% since December of last year. Persistently high core inflation and elevated inflation expectations make the Federal Reserve rate cuts later this year less likely.

As of 5/31/23. Data provided by Bloomberg, NorthCoast Asset Management, Federal Reserve History.

1 The NorthCoast Navigator is a market barometer displaying NorthCoast's current U.S. and international equity exposure and outlook. This aggregate metric is determined by multiple data points across four broad market-moving dimensions: Technical, Sentiment, Macroeconomic, and Valuation. The daily result determines equity exposure in our tactical strategies.

NorthCoast Asset Management is a d/b/a of, and investment advisory services are offered through, Connectus Wealth, LLC, an investment adviser registered with the United States Securities and Exchange Commission (SEC). Registration with the SEC or any state securities authority does not imply a certain level of skill or training. More information about Connectus can be found at www.connectuswealth.com.

NorthCoast and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

PAST PERFORMANCE DOES NOT GUARANTEE OR INDICATE FUTURE RESULTS.

This material should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or investment products or to adopt any investment strategy. The reader should not assume that any investments in companies, securities, sectors, strategies and/or markets identified or described herein were or will be profitable and no representation is made that any investor will or is likely to achieve results comparable to those shown or will make any profit or will be able to avoid incurring substantial losses. Performance differences for certain investors may occur due to various factors, including timing of investment. Investment return will fluctuate and may be volatile, especially over short time horizons.

INVESTING ENTAILS RISKS, INCLUDING POSSIBLE LOSS OF SOME OR ALL OF THE INVESTOR'S PRINCIPAL.

The investment views and market opinions/analyses expressed herein may not reflect those of NorthCoast as a whole and different views may be expressed based on different investment styles, objectives, views or philosophies. To the extent that these materials contain statements about the future, such statements are forward looking and subject to a number of risks and uncertainties.

NorthCoast Asset Management

One Greenwich Office Park, Greenwich, CT 06831, United States