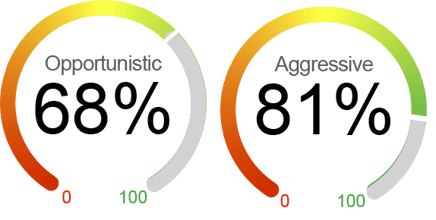

Current Equity Exposure

We employ two distinctive dynamic market exposure models in our strategies: one tailored for growth-focused investors seeking aggressive opportunities and another designed for those with a more defensive approach, prioritizing capital preservation. *For illustrative purposes only.

The US equity market continued to post solid gains in July with the S&P 500 Index reaching new all-time highs, returning 2.4% for the month. Tech and growth stocks led the gains as the “Magnificent 7” rebounded after a pullback earlier in the year due to trade and tariff headlines, and the Nasdaq composite advanced 3.9% for July. We are encouraged by the progress on trade negotiations, the relatively solid Q2 corporate earnings results, and optimism over potential Federal Reserve rate cuts in the second half of the year. Also, a weakening US dollar and pro-business fiscal measures can help to improve business sentiment. While the market is near record highs, we see downward risks in the near term. Uncertainty around the tariff policy could lead to more potential pressure on inflation and a drag on economic growth. Investors are also concerned about weakening consumer consumption and the possibility of delays in monetary easing from the Fed. Furthermore, equity valuations are more stretched after the substantial market gain recently. With this backdrop, we are cautiously optimistic about the US equity market and have increased equity exposure to 69% in our defensive, tailored approach.

What's Driving the Markets?

Tariff Policy Developments: The US equity market has recently digested a slew of tariff news, with partial resolutions such as the trade agreement with EU countries, helping to boost investors’ sentiment. On July 27, President Trump announced that most European imports will be subjected to a 15% tariff, lower than the previously threatened 30% tariff rate. Also, a trade agreement was reached with Japan, which includes a 15% tariff on Japanese imports. On July 29, the US and China concluded another round of trade talks without a final agreement, but officials signaled a possible extension of 90 days after the current “tariff truces” expire on August 12. Although there have been some positive developments in trade negotiations lately, the full effect of tariffs is still unclear. The possibility of additional trade talks or policy changes in August introduces another layer of uncertainty.

Corporate Earnings: As of July 25, among the 34% of S&P 500 companies that have reported Q2 results, 80% have reported a positive EPS surprise, and 80% have reported a positive revenue surprise. The blended YOY earnings growth for the S&P 500 is 6.4%. If 6.4% is the actual growth rate for the quarter, it will mark the lowest earnings growth rate reported by the index since Q1 2024 (5.8%). Although it is still early in the second-quarter earnings season, initial results from major banks have been positive, with the big banks showing ongoing loan growth and stable deposits, indicating that both consumers and businesses continue to borrow actively. Additional signs of consumer strength can be found in earnings reports from travel and leisure companies such as Carnival Corporation. Meanwhile, the recent passage of the “One Big Beautiful Bill” helped to resolve uncertainty around expiring provisions, providing a modest boost to corporate cash flows and capital spending incentives.

Fed Policy: As anticipated, the Federal Open Market Committee kept the Fed funds rate unchanged at 4.25% to 4.5% in July for the fifth consecutive meeting. Despite the modest increase in inflation, the fast shifts in trade policy and unclear business response to the policies have made it difficult to forecast near-term economic trends. The decision was not unanimous, though. Governor Waller, one of two dissenters, argued for an immediate rate cut, citing weak consumer spending and a lack of inflation momentum. At a post-meeting press conference, Fed Chair Powell explained the decision to maintain the rates, noting that the US economy does not appear to be held back by current monetary policy, as the labor market is basically in balance with slower hiring and immigration-limited labor supply growth. Significant uncertainty around inflation, especially from shifting trade policy, further justified the pause. Firms have initially absorbed tariff costs to avoid price hikes. However, as trade agreements with the EU and Japan now reveal a 15% tariff floor, consumer prices are expected to rise as pre-tariff inventories deplete. Looking ahead, we expect a quarter-point rate cut at the Fed’s September FOMC meeting.

By the Numbers

Valuation

|

Sentiment

|

Technical

|

Macroeconomic

|

.jpg)