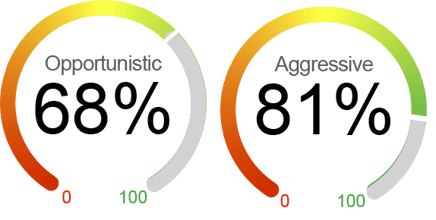

Current Equity Exposure

We employ two distinctive dynamic market exposure models in our strategies: one tailored for growth-focused investors seeking aggressive opportunities and another designed for those with a more defensive approach, prioritizing capital preservation. *For illustrative purposes only.

The US equity market finished August mixed, with the S&P 500 climbing 2.0%, the Dow up 3.4% and the tech-heavy Nasdaq up 0.2%. The Dow’s outperformance and Nasdaq’s slight lagging reflected investor rotation toward cyclical and value-oriented stocks and renewed profit-taking in mega-cap tech and growth names. Tariffs and trade development were mostly overshadowed by economic news and hope about the Fed’s rate cuts for much of the month. The softening labor market and Chairman Powell’s speech at Jackson Hole’s symposium fueled bets that the Fed is likely to lower the policy rate at its September meeting. As of August 31, the Fed funds futures market forecasts with an 88% probability that the Fed will reduce the fed fund rate, compared with a 40% probability at the end of July. We continue to see downward risks in the near term. Uncertainty around tariff policy could lead to more potential pressure on inflation and a drag on economic growth. Recent inflation reports have shown building inflationary pressures, and we expect the trend to continue in the near future due to higher tariffs, a backdrop that the Fed has to balance with a deteriorating labor market. Although the market has interpreted Chairman Powell’s remarks at the Jackson Hole symposium as opening the door to a rate cut in September, we believe that continued caution from the Fed against immediate easing could trigger market volatility. Furthermore, equity valuations are still stretched. With this backdrop, we are cautiously optimistic about the US equity market and have maintained the equity exposure 68% in our defensive, tailored approach.

What's Driving the Markets?

Inflation: The July US inflation data indicate that both the Consumer Price Index (CPI) and Producer Price Index (PPI) came in hotter than expected. The headline CPI rose 0.25% monthly and 2.7% year-over-year in July, while the Core CPI (excluding food and energy) gained 0.3% over the month and accelerated to 3.1% annually, the fastest pace in five months. Tariff-sensitive goods—such as household furnishings, tires, sporting goods, and electronics experienced another sharp increase in July after gains in June. Vehicles have been the exception so far, but we expect their prices to accelerate with 15% tariffs on major car-exporting countries. PPI also surged 0.9% in July, marking a 3.3% year-over-year increase, significantly above expectations, and the largest 12-month gain since February. Notable spikes included roasted coffee (up 30% annually), beef and veal (up over 10% since March), vegetables (up 40% from June to July), and electronics and appliances. Although inflation is accelerating, its long-term trajectory remains unknown due to trade policy uncertainty and moderating demand due to a softening labor market.

Labor Market: The July employment report indicated a sharp deterioration in the labor market, with payroll employment gaining a modest 73,000 in July and massive downward revisions to May and June data totaling 258,000, bringing the three-month average down to only 35,000. The unemployment rate rose marginally to 4.2% and the labor force was shrinking, with the labor participation rate decreasing to 62.2%. While hiring has slowed significantly, layoffs have also started to climb. Initial jobless claims rose to 235,000 for the week ending August 16 after staying between 215,000 and 258,000 since early July. Continuing jobless claims also trended higher, indicating workers had a more difficult time landing new jobs. The July payroll report strengthened our view that the Fed would cut rates at its September meeting, though the Fed remains in a challenging position to respond to both labor market weakness and manage inflationary pressures from rising tariffs.

Fed Policy - Jackson Hole: For the week of August 22, all eyes were on the Fed’s annual conference in Jackson Hole, especially Fed Chair Powell’s final speech. Powell signaled that the Fed is likely to cut interest rates at the FOMC’s September meeting, though that is not guaranteed. He remarked that, “with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.” While Powell did not explicitly endorse an immediate rate cut, his remarks reflected heightened downside risks for employment, even amid persistent inflation pressures. Powell suggested that there is a “reasonable base case” that the effects of tariffs would be “short lived,” resulting in a “one-time shift in the price level” that would not justify higher interest rates. The market responded positively to the speech, interpreting Powell’s remarks as opening the door to a rate cut in September. In an immediate reaction to the speech, the futures market forecast that the Fed will lower the fed fund rate with an 87% probability, compared with a 40% probability at the end of July. Major indexes jumped more than 1.5%, with the S&P 500 reversing a five-day slide.

By the Numbers

Valuation

|

Sentiment

|

Technical

|

Macroeconomic

|

.jpg)