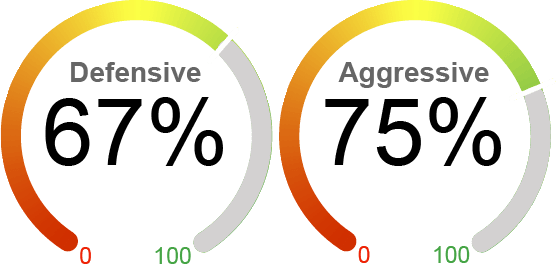

Current Equity Exposure

We employ two distinctive dynamic market exposure models in our strategies: one tailored for growth-focused investors seeking aggressive opportunities and another designed for those with a more defensive approach, prioritizing capital preservation. *For illustrative purposes only.

The U.S. equity market experienced significant volatility in March, with major indexes continuing their downward trajectory. The S&P 500 Index and the Dow declined 5.6% and 4.1%, respectively, while the tech-heavy Nasdaq experienced a more significant loss of 8.1%. Policy uncertainty has undermined investors' confidence in U.S. economic growth and the equity market's strength. Consumer confidence was dampened by a jump in inflation expectations and a softening labor market, evidenced by sharp declines in both the University of Michigan survey as of 03/31/2025 and Conference Board's consumer confidence index. Looking ahead, we believe that policy uncertainty is far from over as the market navigates the murky landscape of tariffs. We have also downgraded our estimate of U.S. growth due to the potential impact of new tariffs and trade tensions, shifting Fed policy, moderating labor market, and slower consumer spending. In terms of equity positioning, we underweight tech, discretionary, and high-beta names as we believe that the growth stocks, including the Mag-7, are unlikely to make a sustainable recovery in the near future, given the still high positioning and concentration risk. With the market corrections, we have taken the opportunity to selectively increase exposure from 61% to 67% in our defensive tailored approach. We stay cautious, however, as we anticipate more market volatility in the near term with still high equity valuation, waning AI optimism, growth concerns, and heightened policy uncertainty.

What's Driving the Markets?

Inflation Concerns: The February CPI (Consumer Price Index) showed some sign of moderation after a concerning spike of 0.5% in January, with the headline CPI rising 0.2% monthly, lowering the annual rate from 3.0% to 2.8%. The core CPI (excluding food and energy) also came in lower than expected, increasing 0.2% month over month and down to 3.1% annually. Food prices eased from 0.4% to 0.2%, and shelter inflation remained in line with our prediction, with the owners' equivalent rent moderating to 0.28% from 0.31% in the previous month. Shelter inflation could be a driver for disinflation if it remains modest, given its significant weight in the CPI. However, the Fed's preferred inflation measure, core PCE (personal consumption expenditure), rose 0.4% in February, lifting the annual rate from a revised 2.7% to 2.8%. The outlook for U.S. inflation gets more complicated due to trade policy uncertainty. According to the final estimate from the University of Michigan consumer sentiment survey, the one-year inflation expectations accelerated to 5.0% from 4.3%, and the five-year expectations rose to 4.1% from 3.5% in February. Although the Fed is likely to view tariff-induced price increases as "transitory," the expectation for an economic downturn is looming with rising production costs and reduced consumer discretionary spending. As a result, the risks could shift from high inflation to slow growth, leading to the Fed's interest rate cut to boost the economy.

Fed policy: As widely expected, the Federal Reserve held its policy rate unchanged at 4.25% - 4.5% in its March meeting. The latest Summary of Economic Projections shows a boost in inflation forecast, with the median PCE estimate rising to 2.8% from 2.5% in its March meeting. However, the Fed officials still indicated two 25bps cuts this year, no change from the projections in the December meeting, owing to lower expectations for economic growth. The median expectation for real GDP was downgraded to 1.7% in March from 2.1% in December. Although economic uncertainty was a key theme at the press conference, Chairman Powell stated that the committee's base case is that tariff-related price pressure will be "transitory." We see risks associated with this "transitory" assumption: an intensifying trade war could lead to retaliatory policies that increase the prices of a wider range of products, potentially causing inflation expectations to become unanchored.

Policy Uncertainty: There have been several significant tariff developments in March 2025, including a 25% tariff on steel imports and a 25% tariff on aluminum imports, an additional 25% tariff on goods from Canada and Mexico that do not satisfy the U.S.-Mexico-Canada Agreement (USMCA) rules of origin, an increase from 10% to 20% for goods from China, announcement of a 25% tariff to major imported automobile part, foreign cars and light trucks. Reciprocal tariffs are also expected to start on April 2. As tariff uncertainty has grown, the stock market has declined recently, reversing all its post-election gains. Stocks of the Big Three U.S. automakers - Ford, General Motors, and Stellantis - all sank after President Trump announced new auto tariffs. Slower growth is expected with higher tariffs as they reduce consumer purchasing power, increasing domestic production costs and negatively impacting exporters as other countries respond with retaliatory measures. Additionally, policy uncertainty could weigh on household consumption and delay business spending and hiring.

By the Numbers

Valuation

|

Sentiment

|

Technical

|

Macroeconomic

|