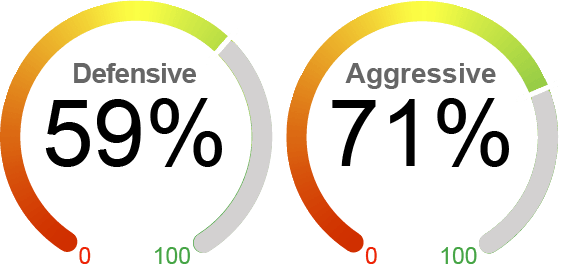

Current Equity Exposure

We employ two distinctive dynamic market exposure models in our strategies: one tailored for growth-focused investors seeking aggressive opportunities and another designed for those with a more defensive approach, prioritizing capital preservation.

Major indexes finished February lower, with the S&P 500 Index and the Dow declining 1.3% and 1.4%, respectively, while the tech-heavy Nasdaq experienced a bigger loss of 3.9%. Markets have been volatile this month as investors digested the Fed's January minutes, a slew of mixed economic and sentiment data, a fresh round of Trump administration tariff proposals, and corporate earnings reports. The minutes from the Fed's January meeting revealed that the policymakers are concerned about upside risks to inflation due to the potential impact of new immigration and tariff policies. In February, consumer confidence plummeted, according to both the Conference Board's consumer confidence index and the University of Michigan's survey, as consumers are worried about stubborn inflation and the potential negative impact of public policy. Downside risks remain, including rich equity valuations, geopolitical tensions, and policy and trade uncertainties. Although Q4 earnings reports have been very strong overall, the valuation premium of US equities compared to international equities is significantly higher than its historical level, with forward P/E currently 50% above the rest vs. the historical level of 10%. Meanwhile, the Mag-7 and US Tech sector are not performing as exceptionally as before, with concerns about AI investments and increased competition from China. With this backdrop, we have a relatively conservative stance on US equity and have slightly decreased our allocation in our defensive tailored approach from 61% to 59%.

What's Driving the Markets?

Tariff and Policy Uncertainty: President Trump has recently announced a variety of new tariffs as part of his "America First" trade policy. On February 1, President Trump announced 25% tariffs on all imports from Canada and Mexico and a 10% tariff on all imports from China. The tariffs on Chinese imports took effect on February 4, while the tariffs on Canada and Mexico are scheduled for March 4 after a 30-day suspension. Additionally, on February 10, President Trump signed proclamations to expand existing Section 232 tariffs on steel and aluminum, ending all current exemptions and increasing the aluminum tariff rate from 10% to 25%. The administration also unveiled the "Fair and Reciprocal Plan" and has announced plans to impose tariffs on auto imports, potentially at a rate of 25%. These actions have led to market volatility as investors worried about the potential economic impacts. 1) impact on GDP: While the precise impact of tariffs on US GDP is still difficult to forecast, rough estimates indicate that real GDP could be reduced by about 0.5% to 0.6% in the next 12 months, driven by a decline in households' purchasing power, increased investment uncertainty, and a negative impact on US exporters. 2) potentially increase inflation: according to analysis from Federal Reserve Bank of Boston, the 10% tariff on China and the 25% tariffs on Canada and Mexico could add up to 0.8% increase of core inflation. 3) impact on equity valuation: tariffs could reduce the fair value of US equity through its negative impact on profit margin due to rising input costs, slowing sales, and a hit on exports.

Inflation Concerns: The January CPI (Consumer Price Index) accelerated, with the headline CPI climbing 0.5% monthly, pushing the annual rate from 2.9% to 3.0%. The core CPI (excluding food and energy) also came in sticker than expected, increasing 0.4% month over month and up to 3.3% annually. The increase in CPI was broad-based, including a 0.5% rise in food inflation, with egg prices surging 15% due to bird flu. Used vehicles experienced the largest monthly increase since late 2022, probably due to concerns over tariffs on steel and aluminum. The good news is that shelter inflation rose by 0.3%, which could be a driver for disinflation if it remains modest. Meanwhile, producer prices increased more than anticipated, with PPI for final demand rising by 0.4% and the annual rate remaining at 3.5%. What is also concerning is that inflation expectations soared in the recent two months, indicating that consumers are worried that tariffs could have a material impact on inflation. According to the final estimate from the University of Michigan consumer sentiment survey, the one-year inflation expectations jumped to 4.3% from 3.3%, and the five-year expectations rose to 3.5% from 3.2% in January.

European Equity Outperformance: While US equities have long outperformed international market equities, the European equity market started the year strong, and the positive trend continued into February. The Stoxx 600 index, which includes various European stocks, climbed 10% year to date, compared to 1.4% for the S&P 500. We believe that the strong outperformance is due to several key factors: 1) valuation advantage. European stocks are trading at a significant discount compared to their US counterparts. The price-to-earnings ratio for the Stoxx 600 index stands at 15.4, a discount of over 36% compared to the S&P 500 with P/E of 23.9, making European equities more attractive. 2) Potential easing of tension in the Ukraine conflict. A peace agreement could further reduce European energy prices, easing inflation and fostering economic growth in Europe. 3) Monetary Policy Expectations: given the still sluggish growth and easing inflation in Europe, more aggressive interest rate cuts are expected in Europe compared to the US, with anticipation of 100 basis points of cuts versus only 25 basis points in the US this year.

By the Numbers

Valuation

|

Sentiment

|

Technical

|

Macroeconomic

|