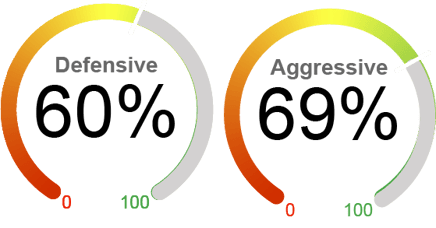

Current Equity Exposure

We employ two distinctive dynamic market exposure models in our strategies: one tailored for growth-focused investors seeking aggressive opportunities and another designed for those with a more defensive approach, prioritizing capital preservation. *For illustrative purposes only.

April 2025 was defined by tremendous equity market volatility, driven primarily by new tariffs and resulting trade uncertainty. Economic data pointed to a slowdown, with the first quarterly GDP contracted by 0.3%, deteriorating business and consumer sentiment, and mixed signals on inflation. While markets rebounded from intra-month lows on hopes for trade negotiations and upcoming earnings, major indexes closed April mixed. The S&P 500 Index and the Dow declined 0.7% and 3.1%, respectively, while the tech-heavy Nasdaq finished the month with a slight gain of 0.9%. Policy uncertainty has undermined investors' confidence in U.S. economic growth and the equity market's strength. Consumer confidence was dampened by a jump in inflation expectations and a softening labor market, evidenced by sharp declines in the University of Michigan survey and the Conference Board's consumer confidence index. The month also saw high-profile earnings reports from major tech firms, which drew investor focus. While some consumer staples outperformed on strong earnings, other sectors, such as energy and technology, lagged due to tariff headwinds and cautious guidance. Looking ahead, we believe investors still face downside risks from policy uncertainty and potential economic slowdown. With the market rebound later in the month, we have taken the opportunity to trim equity exposure from 67% to 60% in our defensive tailored approach. We still stay cautious, however, as we anticipate more market volatility in the near term with still high equity valuation, waning AI optimism, growth concerns, and heightened policy uncertainty.

What's Driving the Markets?

Tariff Policy: April 2025 marked a dramatic escalation in U.S. tariff policy and tremendous market volatility. Although a 90-day suspension of most "reciprocal" tariffs was announced on April 2, a 10% baseline tariff on imports from most countries remains in effect. Also, China faced a tariff rate of up to 145% on most imports, and China has imposed a 125% retaliatory tariff on U.S. goods. We believe the intensifying trade conflicts will significantly impact 1) economic growth: The heightened trade barriers will likely increase inflation and reduce consumption, investment, and export. The Atlanta Fed's GDPNow model published on April 24 predicts a contraction of US GDP by an annualized rate of -2.5% in Q1 2025. 2) trade disruptions: the U.S. and China trade is basically at a standstill. The immediate impact will be price increases for imported goods from China, ranging from clothing to cell phones, and a hit to sales to US manufacturers and farmers exporting to China. 3) Higher inflation: The average effective tariff rate for U.S. consumers is now 27%, which is expected to increase the overall price level by 2.9% in the short run, or a 1.7% price increase adjusted by consumer purchasing habits. 4) equity valuation: tariffs could reduce the fair value of U.S. equity by negatively impacting profit margin due to rising input costs, slowing sales, and a hit on exports.

Inflation Concerns: As widely expected, the Federal Reserve held its policy rate unchanged at 4.25% - 4.5% in its March meeting. The latest Summary of Economic Projections shows a boost in inflation forecast, with the median PCE estimate rising to 2.8% from 2.5% in its March meeting. However, the Fed officials still indicated two 25bps cuts this year, no change from the projections in the December meeting, owing to lower expectations for economic growth. The median expectation for real GDP was downgraded to 1.7% in March from 2.1% in December. Although economic uncertainty was a key theme at the press conference, Chairman Powell stated that the committee's base case is that tariff-related price pressure will be "transitory." We see risks associated with this "transitory" assumption: an intensifying trade war could lead to retaliatory policies that increase the prices of a wider range of products, potentially causing inflation expectations to become unanchored.

Economic and Sentiment Data: Although April's hard data (quantitative metrics) has not fully reflected the impact of the new tariff policy, the soft data (survey-based sentiment) are rapidly deteriorating with mounting risks from the new tariff policy, monetary policy uncertainty, and higher inflation expectations. The labor market proved stronger than expected and eased fears of an immediate slowdown, with payroll rising by 228,000. However, the effects of DOGE-driven spending and recent job cuts haven't fully materialized yet. At the same time, consumer confidence plummeted, according to both the University of Michigan's survey (from 57.0 in March to 52.2 in April, the lowest level since July 2022) and the Conference Board's consumer confidence index (from 100.1 in February to 86.0 in April). Housebuilder confidence and small business optimism also continued their downward trend. The leading economic indicator (LEI) also continued to fall, with the Conference Board LEI dropping 0.7% in March, driven by weaker consumer expectations, a sharp decline in stock prices, and softer manufacturing orders. While the LEI does not signal an imminent recession, it points to slowing growth and heightened economic uncertainty.

By the Numbers

Valuation

|

Sentiment

|

Technical

|

Macroeconomic

|